The Crude Oil Price Story: 1861- today

Like most other commodities in the markets, crude oil prices have routinely experienced wild price swings alternating between times of great shortages, high demand and high prices and periods of oversupply, low demand and depressed prices. These so-called crude oil “Price Cycles” tend to last several years, depending on variables such as oil demand, volume of oil drilled, processed and sold by the major producers.

Since the early days of commercial production in Baku, Azerbaijan, these price swings have been triggered by economic and political events, technological advancements and changes within the petroleum industry, and continue to influence prices in the present day.

Source: IG Group

1800-1869: Early black gold rush

The modern oil industry traces back its roots to Baku where the first commercial refinery was established in 1837 to distill oil into paraffin for heating and lighting purposes.

The first modern oil well was sunk in Baku in 1846 and reached a depth of 21 meters. The single oil field accounted for more than 90% of global production, with most of the oil finding its way to Persia (present-day Iran).

Several commercial oil wells soon followed:

- Poland--1854

- Bucharest, Romania--1857

- Ontario, Canada--1858

- Pennsylvania, USA--1859

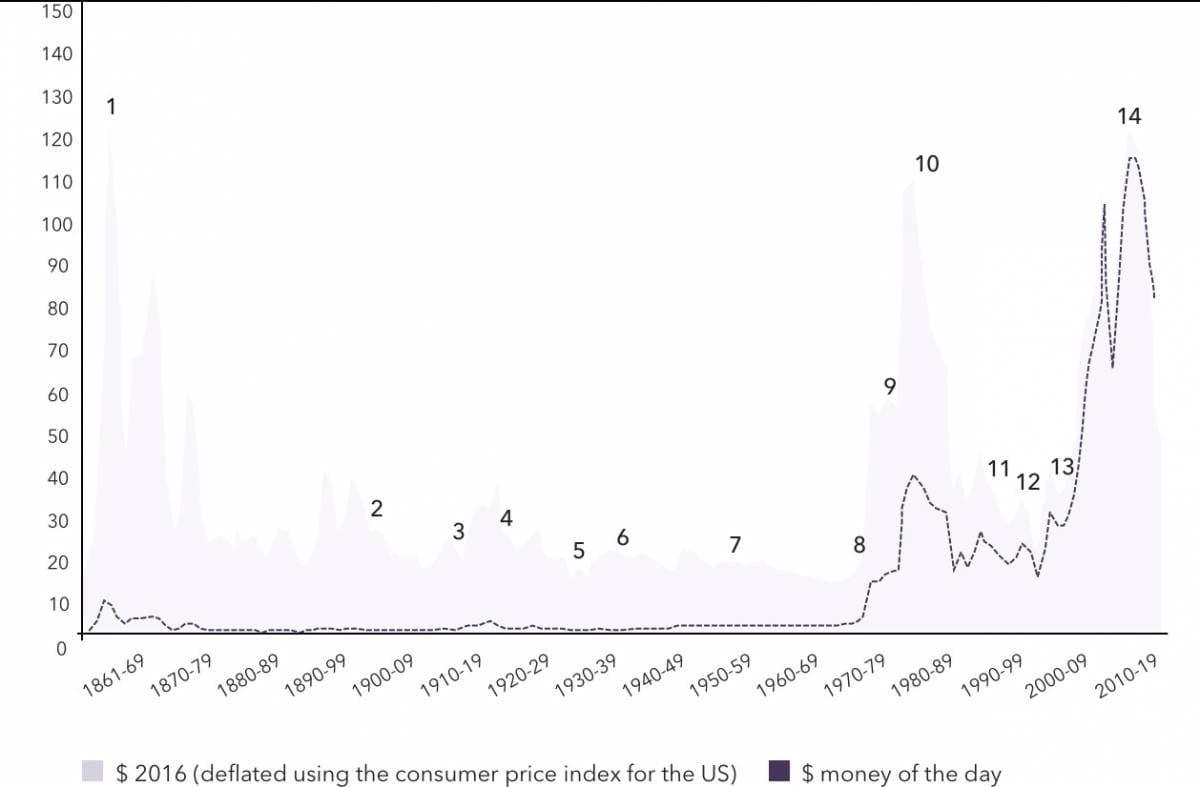

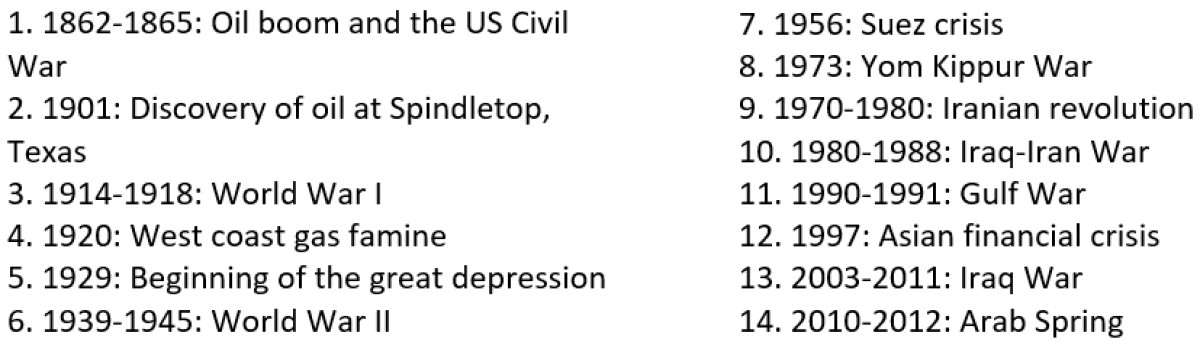

Pennsylvania was the epicenter of the first black gold rush, producing nearly 50% of the world’s oil. Prices shot up rapidly from $0.49 per barrel in 1861 to $6.59 a barrel in 1865, representing a massive 1,245% climb in the space of just four years.

1870-1913: The auto revolution

Whereas some economists contend that the modern oil industry only took off after WWII with the creation of the Marshall Plan - part of which was an agreement for a Free On Board price for all players - others argue that the incorporation of Standard Oil Co by John D. Rockefeller in 1870 in Ohio was the true launchpad for the industry.

Standard Oil quickly rose to prominence over the next two decades, driving down prices and buying up the competition. The company was so successful that it controlled nearly 90% of refined oil in the United States by 1890. As production continued to expand both in the US and in Russia, global oil prices fell from an average of $2.56 a barrel in 1876 to just $0.56 in 1892. This was further accelerated with the launch of the first commercial cars in Germany and the US in 1896, a technological revolution that would fuel unprecedented growth for the industry.

1901-1911: Rise of the oil majors

Many of the modern oil majors can trace their origins to the early 20th century.

- The discovery of oil at Spindletop, Texas, led to the creation of Texaco and Gulf Oil in 1901

- Increasing competitive pressure led to Shell and Royal Dutch merging in 1907 to form Royal Dutch/Shell

- BP, formerly known as the Anglo-Persian Oil Company, was incorporated in 1908 following the discovery of oil in Iran

- Chevron, Exxon and Mobil (now Exxon Mobil) came into being in 1911 after the split of Standard Oil Co following an antitrust ruling by the US Supreme Court

The seven oil majors went on to control 85% of the world’s oil reserves during their golden years in the 1970s.

1914-1949: Oil discoveries, wars, crises

The discovery of oil in Cushing, Oklahoma, in 1912 is considered an important milestone for the US oil industry because the region grew to become one of the most important oil fields in the country. Notably, it also became the settlement point for the West Texas Intermediate (WTI) oil price, a leading global oil price benchmark.

The next four and a half decades were a turbulent period marked by a series of major wars and economic crises, all of which would have an important bearing on oil prices.

First was WWI (1914-1918) which drove up global demand for oil that more than doubled oil prices from $0.81 per barrel in 1914 to $1.98 by the end of the war. Demand continued to grow even after the war ended mainly fueled by the ever-increasing popularity of the automobile and a gasoline shortage in the US west coast. At first, prices surged to $3.07 per barrel before retreating and stabilizing around $1.61 as production increased.

Around this time, oil companies started researching other applications for the commodity including commercial production of plastics. However, prices remained relatively low despite the extra demand created by these applications mainly due to a combination of stiff competition and plentiful supply. Meanwhile, major oil discoveries elsewhere continued to keep the markets awash with the commodity including Venezuela, Iraq, the USSR, Kuwait, Saudi Arabia and the Gulf of Mexico.

The discovery of oil in East Texas in 1930 was one of the major highlights of this period because it helped create an oil glut that happened to coincide with the Great Depression that consequently depressed prices from $1.19 in 1930 to $0.65 in 1931. It took the intervention of the Texas Railroad Commission which enforced production quotas to stabilize prices and prevent further declines.

Just like WWI, the beginning of WWII in 1939 also helped drive demand and boost prices. However, the effect was less pronounced this time around due to bountiful global supply. Nevertheless, the war made governments acutely aware of the need to control reserves, and it would clearly show in their actions over the next couple of decades.

1950-2003: Battle to control production

The ending of the second world war would usher in a period whereby many countries made concerted efforts to hold sway in global oil production, with several governments nationalizing their oil infrastructure.

Between 1950 and1960, Iran, Indonesia and Saudi Arabia all partly nationalized their oil industries. The Suez crisis of 1956-57 saw Egypt seize the Suez Canal through which nearly five percent of the world’s oil flowed.

However, it was the US and USSR that would emerge as the biggest heavyweights in terms of production control. In the late 1950s, the USSR started to flood the market with cheap oil leading to price cuts by the majors in a bid to remain competitive. In response to these developments, Saudi Arabia, Iran, Iraq, Kuwait and Venezuela teamed up and formed OPEC as a means to lower competition between their countries and also as a means to have a bigger impact in controlling supply.

OPEC went on to expand its membership over the next two decades with UAE, Libya, Indonesia, Qatar, Nigeria, Algeria, Gabon and Ecuador joining the organization. Between 1960 and 1976, most of these countries took control of their oil reserves by buying out or forcibly taking shares from the oil majors.

The US and the USSR continued to throw their weight around but soon the influence shifted to OPEC. In 1973, OPEC members embargoed countries supporting Israel in the Yom Kippur war. Consequently, oil prices shot up to levels never witnessed before, from $2.48 per barrel in 1972 to $11.58 by 1974 and even higher in parts of the US.

It was around this time when oil was discovered in the North Sea in a region controlled by the UK and Norway. Oil from this area is referred to as Brent crude and is used alongside WTI to benchmark prices.

Iran sharply cut production during the Iranian revolution (1970-1980) and also during the Iran-Iraq war of 1980-1988 leading to a spike in prices to $36.83. However, prices fell again due to demand shocks as well as increased production by the USSR, which became the world’s largest producer in 1988. Iraq invaded Kuwait in 1990, leading to the Gulf War. This created a major supply shock that led to prices shooting up from $14.98 per barrel before the war to $41.00 in September 1991.

The 1990s witnessed wild price fluctuations. The Soviet Union fell in 1991, precipitating the collapse of the Russian oil sector with production halving over the next decade mainly due to reduced investments. However, global demand also tumbled in 1997 due to the Asian financial crisis but managed to recover by the turn of the century after the region’s economic outlook improved.

This next decade witnessed some of the most spectacular explosions in oil prices.

New Uncertainty & Technology: 2003 - today

The US invaded Iraq in 2003 leading to supply uncertainties. This was further compounded by massive demand growth by Asia and China. Consequently, prices jumped from $28.38 per barrel in July 2000 to $146.02 in July 2008.

From here prices fell due to the global financial crisis of 2008 before staging a comeback. The Arab Spring of 2011 created supply shortages and helped push prices to $126.48 per barrel.

Technological advancements in recent times have significantly altered the global oil landscape. Hydraulic fracturing has pushed the US to the top of the pack once again, reducing the influence of OPEC and depressing prices. Flooding of the market by US shale has led to a sharp drop in global oil prices, from $114.84 per barrel in June 2014 to $28.47 in January 2016. OPEC has tried to ameliorate the glut by teaming up with non-OPEC countries such as Russia to implement production cuts. Consequently, prices have recovered somewhat but have never approached levels seen in the past decade.

The Future?

With the US now acting as the new ‘swing producer’ OPEC’s influence and ability to control prices is likely to remain diminished. The unresolved trade war between the US and China as well as geopolitical uncertainty in Iran, Syria and other countries has helped encourage prices from their 2016 lows of below $30 per barrel to $54.70 in October 2019. But with continued high levels of shale production and a weakening global economy, prices are expected to remain subdued with prices projected to average $66 a barrel in 2019 and $65 a barrel in 2020.

Source: Alex Kimani for Oilprice.com